The digitisation has facilitated the use of plastic money so easily. Previously, it was a time-consuming process to get a credit card, involving manual documentation and several days of waiting to get approved.

But in recent times, getting a credit card has become so fast, taking only a few hours. This ease has resulted in a massive increase in the usage of credit cards. As per The Economic Times, RBI data indicate that outstanding credit cards in the system increased from 55.3 million at the close of 2019 to 108 million in December 2024.

With credit cards becoming a part of our lives, having a good credit score has never been more crucial. Having a good credit score not only makes getting a loan easier, but you can get lower interest rates than the regular interest rate and better terms and conditions. A good credit score can even lead to better job prospects.

Here are some effective measures to help you improve your credit score.

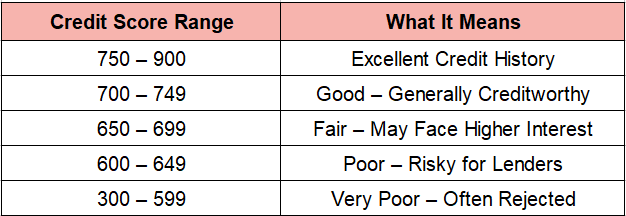

A credit score is a three-digit numerical summary of your credit history. It reflects how responsibly you've managed borrowed money in the past, and it helps banks, lenders, and financial institutions assess the risk of lending you money.

Key Points:

The following are simple ways to improve your credit score.

Your payment record is an excellent factor in defining your credit score. One delayed payment will bring it down. Keep paying your loan EMIs, credit card dues, and your bills on time. You may set reminders or do auto-pay for this purpose. Also, pay the full due amount on time and not just the minimum due.

Credit usage or credit utilisation ratio is the percentage of the credit limit that you are using. Let us say you have a credit card with a limit of ₹1,00,000 and you spend ₹90,000. Your usage is 90%, which is not ideal. Keep your credit usage within 30% or so.

Each time you apply for a new loan or credit card, the lender looks at your credit report. And these requests get reflected in your credit score. Having too many of these within a short period can adversely impact your score. Apply only when necessary.

Regularly monitoring your credit report is essential, as errors can sometimes negatively impact your credit score. You might come across incorrect late payments or accounts mistakenly listed under your name. By reviewing your credit report periodically and reporting any inaccuracies, you can ensure your score remains accurate and improve it if needed.

The longer your history of credit, the higher your score. If you have a credit card and you've made payments on time, keep it active by occasionally using it. Closing old credit accounts might reduce your credit history and your score.

The type of loan you take can also indicate your credit behaviour to the lender. Having too many unsecured loans that are not backed by assets, such as personal loans and credit card dues, can affect your future loan options. Therefore, it is better to choose secured loans, like a home loan or car loan, to demonstrate your creditworthiness to lenders.

If you struggle to pay off your debt, don’t ignore it. Call your bank or lender to negotiate better repayment terms. Many lenders offer flexible plans that can help protect your credit score.

Improving credit takes time, but consistent effort can lead to an improved score. Pay bills on time, manage your credit utilisation, and stay informed about credit. These small actions will help you build a good credit score, making financial transactions more manageable and smoother.